Retainage and contract bonds sit at a busy intersection in construction risk management. If you manage projects, underwrite surety, or negotiate subcontracts, you have felt the friction. Owners use retainage to keep contractors attentive through closeout. Sureties backstop performance and payment to ensure completion when something breaks. Each tool has its own logic, but the two can either complement each other or collide, depending on how the contract is drafted and how the project unfolds in the field.

I have seen retainage save an owner from sloppy turnover, and I have seen it choke a subcontractor’s cash flow to the point of failure. I have also watched a surety step into a job and find itself negotiating over retainage that should have been released months earlier. Those experiences shape the guidance here. If you understand where retainage and a contract bond support the same goal and where they pull in opposite directions, you can make better decisions during contract formation, progress payment reviews, and claims.

What retainage tries to accomplish

Retainage is a holdback. An owner withholds a small percentage of each progress payment until substantial completion or final acceptance. On public work in many states, that number lands between 5 and 10 percent. On private work, it varies more widely, sometimes tiered or capped by statute. The purpose is leverage. If a contractor walks off or slips into complacency at 92 percent complete, retainage gives the owner a financial handle to pull the job across the line.

That leverage extends down the chain. Prime contracts often mirror retainage into subcontracts. Subs carry their own holdbacks to suppliers or lower tier subs, though many states restrict pass-through percentages and timing. Used well, retainage focuses all parties on punch lists, documentation, and commissioning. Used carelessly, it impairs the exact cash flow that funds those tasks.

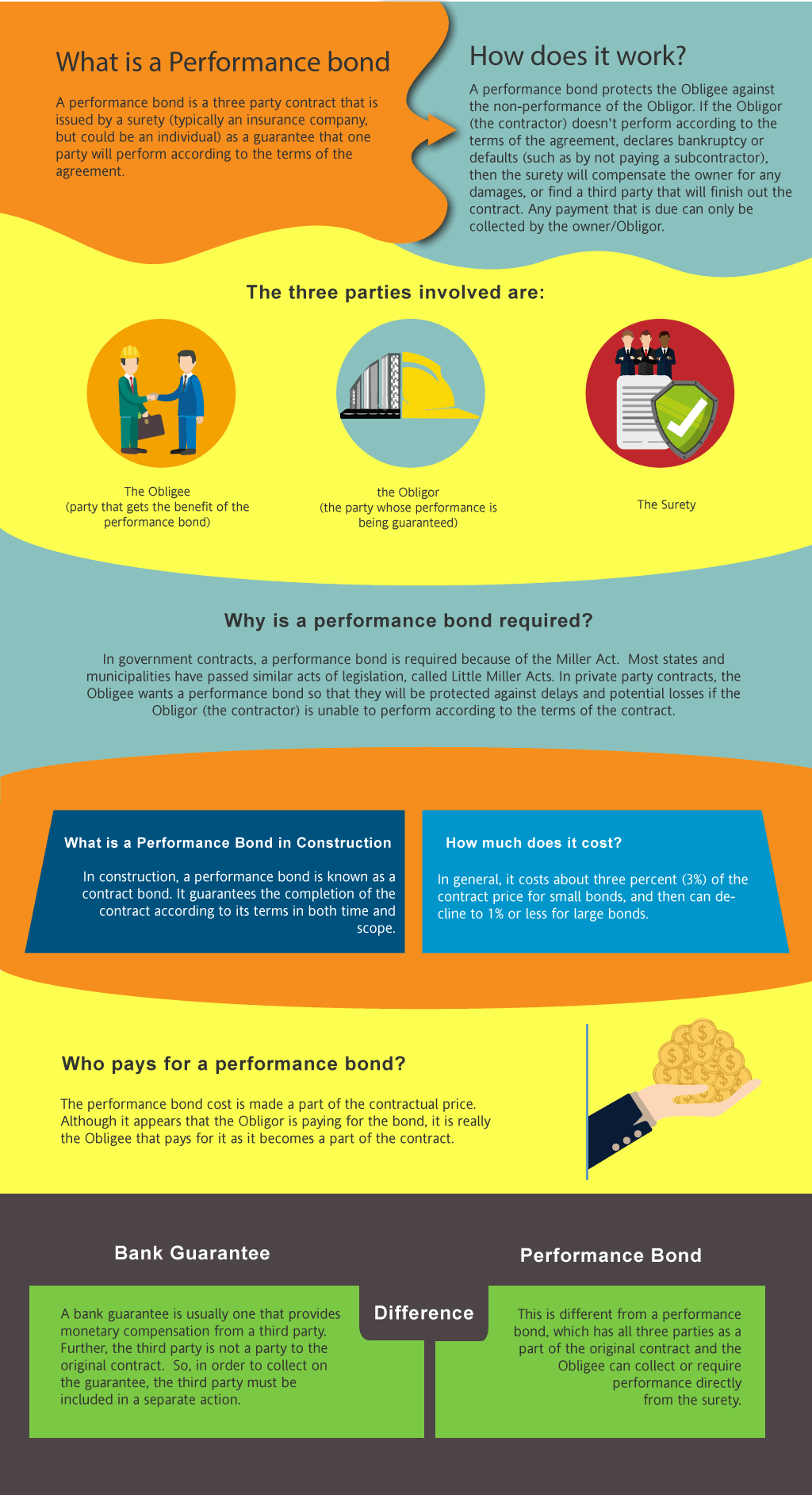

What a contract bond guarantees

A contract bond, commonly referred to as a surety bond, is a three-party risk transfer. The owner (obligee) requires the contractor (principal) to post a bond from a surety company that promises performance and payment according to the contract. The performance bond supports timely, conforming completion. The payment bond protects those furnishing labor and materials. If the contractor defaults, the surety steps in with options: finance the principal, tender a completion contractor, or complete the work itself.

Unlike insurance, surety is fundamentally a credit product. The surety expects to be indemnified by the principal for losses. Underwriters care deeply about contract terms that can spur default or inflate loss, which is why retainage policy shows up in bond reviews. Common forms like AIA A312 and ConsensusDocs furnish structure, but the project’s specific retainage setup, state statutes, and negotiated amendments often override boilerplate.

Retainage and the bond share a goal, but use different levers

Both tools aim to ensure completion and protect funds. Retainage withholds the contractor’s money. A performance bond brings in the surety’s capacity. In an ideal scenario, they complement each other. Moderate retainage maintains attention, while the bond stands behind performance if the contractor fails. Where conflict arises is timing and cash flow. Excessive retainage, or late release of retainage, can push an otherwise capable contractor into distress. That increases the likelihood of a bond claim and, ironically, forces the surety to manage a problem that retainage helped create.

Owners sometimes argue for higher retainage on risky scopes, thinking more leverage equals more control. In practice, I have seen a 10 percent blanket retainage on a $40 million job tie up $4 million of earned cash for months. At peak production, that can mean the difference between paying crews on Friday or drawing on an expensive credit line. One large mechanical subcontractor I worked with carried 8 percent blended retainage across three hospitals at once and watched its borrowing base evaporate during a commissioning crunch. They were profitable on paper, but starved for cash. Their surety raised covenants, which tightened liquidity further. That is how small drafting choices escalate into claims conditions.

The legal character of retainage matters

Retainage is not an owner’s slush fund. It is typically the contractor’s earned money, provisionally withheld per contract terms. The right to retain is bounded by statute and contract language. Some states require retainage to be held in trust or interest-bearing accounts. Others mandate automatic reduction of retainage at defined milestones, like 50 percent completion of the contract, or upon acceptance of discrete portions of the work. These details affect bond exposure directly. When a default occurs, a surety assesses available contract balances, unpaid progress estimates, and withheld retainage to determine completion funds. Misapplied retainage can narrow that pool and complicate the surety’s options.

On public projects governed by the federal Miller Act, the payment bond protects subcontractors and suppliers, but federal law does not cap retainage. Many federal agencies adopt FAR clauses and internal policies that reduce or eliminate routine retainage when performance is satisfactory, which helps with cash flow. State Little Miller Acts vary widely. If you run multi-state work, do not assume the same retainage playbook applies everywhere. A surety will not.

Where retainage meets performance bond duties

When a contractor defaults, the surety looks at the remaining contract balance, including unreleased retainage, as the primary source to fund completion. If retainage is improperly withheld or already used to pay unrelated owner costs, the surety loses a key resource, which can slow resolution or increase the likelihood of litigation. Conversely, if the owner has held excessive retainage beyond what the contract or statute allows, the surety may insist on releasing part of it to re-mobilize the defaulted principal or to fund a tendered completion contractor.

Consider a mid-rise residential build where the owner kept 10 percent retainage even after substantial completion and occupancy. The general contractor stumbled on closeout documentation and a handful of punch list items worth perhaps $150,000. Retainage stood at $2.1 million. The GC’s lender tightened the spigot, payroll wobbled, subs slowed their return visits, and the schedule drifted another two months. Eventually the owner declared default to wake up the GC. The surety stepped in, saw that retainage dwarfed the cost to cure, and demanded a targeted release to pay subs for closeout work under a surety-supervised plan. The owner agreed, but the delay cost more than the original dispute. A balanced retainage plan and earlier partial releases would have avoided the standoff.

Payment bonds, retainage, and subcontractor rights

Subcontractors often carry the heaviest retainage burden with the leanest cash reserves. Payment bonds protect them if the prime contractor fails to pay for properly performed work. But the bond does not guarantee early release of retainage unless the subcontract and applicable law require it. Trouble starts when a prime sits on retainage long after the sub’s scope is complete and accepted. In several states, prompt pay statutes force release of a sub’s retainage once its portion is done, even if the overall project remains in progress. If the prime ignores that rule and later tips into default, the surety can face a cluster of payment bond claims centered on retainage that should have been released earlier.

I worked through a case where a specialty façade subcontractor finished nine months ahead of project completion. The prime kept full retainage, citing “project-wide closeout,” while clocking daily liquidated damages against the GC for unrelated delays. The sub filed a payment bond claim for retainage after 30 days of inaction beyond the statutory release window. The surety investigated, confirmed acceptance of the sub’s scope, and pushed the GC to pay. Payment arrived, but not before the sub bled out $600,000 of working capital. It took another project cycle to recover. Clear subcontract language aligning with state release rules, plus project-specific retainage caps for early-finishing trades, would have reduced risk for everyone, including the bond underwriter.

Retainage reduction techniques that ease bond risk

There is a middle path between no retainage and punitive holdbacks. Owners and primes can tailor retainage to the shape of the work. I have found three practices especially effective on complex jobs: milestone-based reductions, early release for discrete scopes, and retainage caps by tier.

Milestone-based reductions convert a flat percentage into a trajectory. Start at, say, 10 percent for the first third of the job, drop to 5 percent once core and shell is weather-tight, then to 2.5 percent at substantial completion. That plan aligns with risk: earlier phases have more unknowns, whereas late work revolves around punch and commissioning. It preserves leverage without strangling cash at peak manpower.

Early release for discrete scopes comes up on projects with distinct packages like site utilities, structural steel, or curtainwall. If the inspection and warranties are in place and the owner has accepted the segment, hold only a nominal warranty reserve or none at all, depending on statute and contract. This keeps specialty subs liquid and reduces payment bond claim risk.

Retainage caps by tier place a project-level ceiling on total retainage withheld from each subcontractor. For example, cap at 5 percent of that sub’s contract value, regardless of changes. Caps prevent runaway retainage when change order volume spikes late in the job. On one airport concourse, a mechanical sub whose original contract was $18 million grew to $28 million with owner-driven scope. Without a cap, retainage would have jumped from $900,000 to $1.4 million during startup, exactly when technicians and commissioning agents were billing premium time. A negotiated $1 million cap, paired with a testing and balancing signoff trigger, kept them solvent, which kept the surety calm.

How sureties view retainage in underwriting

Surety underwriters parse retainage policy the same way lenders read loan covenants. They look for triggers that can drain cash or invite disputes. A few questions recur in credit memos. What retainage percentage applies at each tier? Are there statutory limits or mandatory reductions? Who controls release, and what objective criteria, if any, govern approval? Does the contract allow partial release for early scopes? Are there owner-friendly offsets or cross-defaults that could trap retainage? What form of certification closes out retainage: architect’s certificate, inspector signoff, commissioning reports, or all three?

Underwriters also compare retainage with other risk signals, like liquidated damages, schedule buffers, contractor’s working capital, and the concentration of critical path trades. A contractor carrying thin cash against high retainage and high LDs sets off alarms. Conversely, a contractor with robust working capital, a reasonable retainage schedule, and a cooperative owner often earns higher bond capacity. The message is consistent: balanced retainage supports better bond terms.

Retainage during a default: practical sequencing

When https://sites.google.com/view/swiftbond/surety-bonds/consequences-of-not-adhering-to-exclusions-and-limitations-of-surety-bond a default is declared, sequencing matters more than theory. The surety needs control of funds that the contract allocates to completion, including retainage. Owners often want to net out perceived damages straight from retainage, then invite the surety to finish the work with whatever remains. That approach leads to disputes. A smoother path follows the contract’s framework and keeps the completion fund intact until an agreed-upon plan takes shape.

Here is a concise sequence that has worked repeatedly in the field:

- Establish the completion fund. Confirm unpaid progress, approved change orders, and retainage balances. Segregate the money. Agree on scope to finish. Define open work, punch items, and warranty completions with a shared log. Select the completion option. Finance the principal if viable, tender a completion contractor, or use a takeover. Document who does what and when. Release retainage strategically. Pay subs for verified closeout work and materials. Tie releases to deliverables like O&M manuals, test reports, or occupancy. True up damages separately. Once the job is complete, calculate delay costs or backcharges using the contract’s dispute process, not unilateral retainage raids.

This structure protects the owner’s leverage while giving the surety the runway to complete efficiently. The payment bond stays in the background unless lower tier parties remain unpaid, which is less likely if retainage flows to the right hands at the right time.

Warranty risk and the myth of perpetual retainage

Owners sometimes cling to retainage far past substantial completion to protect against latent defects. That is tempting but misguided. Warranty obligations are better enforced through clear warranty clauses, bonds that specifically cover maintenance where customary, and quick response provisions with defined cure periods. Retainage is a blunt instrument for long-tail risks. Most statutes and industry forms contemplate retainage release near final acceptance, not years later. If an owner insists on extended financial security, maintenance bonds or limited warranty bonds tailored to the exposure do a cleaner job than frozen progress money.

I recall a campus utility project where the owner held 5 percent retainage for the entire two-year warranty term to guard against seasonal failures. Predictably, the contractor priced that risk into the bid. The owner paid more up front, then fought constantly over whether a given repair justified another month of retained funds. A small, separate maintenance bond would have cost a fraction and avoided the operational friction.

Accounting and tax effects that ripple into bonding

Contractors working under percentage-of-completion accounting recognize retainage as an earned receivable, not revenue. On the balance sheet, retainage shows up as a separate line under contracts receivable. If retainage grows, working capital and cash flows get squeezed even if the job is profitable. Surety analysts look at the aging of retainage, not just the total. Retainage older than 120 or 180 days signals closeout issues or owner disputes. It can trigger adjustments to bonding capacity. On multi-project contractors, a pattern of slow retainage release across several owners often correlates with poor document control more than field quality. Tighten submittal logs, commissioning plans, and turnover packages, and bonding improves.

Tax timing also matters. While most retainage is part of the contract price for tax purposes when billed or earned, cash-based taxpayers feel the difference acutely, and some states have peculiar gross receipts rules. If you are bidding a high retainage job with thin margins, forecast the tax and cash consequences together or you may borrow just to pay taxes on money that sits in someone else’s account.

Drafting tips for owners, contractors, and sureties

Clarity in the prime contract and subcontracts pays dividends. I prefer retainage clauses that specify percentage, caps, objective reduction triggers, and the documentation required for release. The triggers need not be complicated. Tie reductions to receipt of permanent power, enclosure, start of commissioning, issuance of certificate of substantial completion, and final completion. Spell out that acceptance of discrete scopes allows partial retainage release. Identify the decision maker for each step, and require written reasons for any denial within a short window. Include a prompt pay reference if your jurisdiction has one, along with any trust or interest requirements for retained funds.

For subcontracts, mirror the prime retainage structure but avoid compounding holdbacks. If the owner holds 5 percent from the prime, there is rarely justification for the prime to hold 10 percent from subs. Add early release rights for subs whose scopes end before project completion. Include a clear pathway for payment bond claims tied to retainage if statutory release deadlines pass. That clause motivates timely action and helps the surety intervene before relationships sour.

Sureties can help by flagging aggressive retainage terms during bond underwriting. If a bid package calls for 10 percent retainage with no reductions on a 36-month job layered with heavy LDs, the underwriter should ask the owner to adopt a reduction schedule or cap. Many owners will agree, especially if the contractor shows how the change lowers completed cost risk and speeds closeout.

Edge cases where retainage and bonds behave differently

Design-build and CM-at-risk projects compress roles, which can distort retainage logic. When the contractor also holds design risk, owners sometimes argue for higher retainage to offset potential redesign or rework. Given that design liability extends through professional liability, not just construction performance, excessive retainage duplicates security and encourages claims friction. Better to define design milestone swiftbonds acceptances and tie retainage reductions to them, paired with appropriate professional liability terms.

Unit price and heavy civil jobs present another twist. Weather windows, changeable quantities, and long punch lists for environmental compliance give owners a reason to hold leverage late. Many DOTs use retainage sparingly or not at all, relying on stringent inspection and progress estimates to manage quality. Where retainage does apply, agencies often reduce it to as low as 2 percent near the end and release for completed sections open to traffic. Payment and performance bonds remain the backbone for default risk. The workable balance there is instructive for vertical projects.

On fast-track interiors, especially with landlord-tenant dynamics, the landlord may hold retainage while the tenant’s opening date sets a hard deadline. If the landlord sits on retainage after the tenant opens, the GC has little leverage. In those cases, I push for an escrow mechanism that auto-releases retainage upon certificate of occupancy, subject to a short punch list period. The performance bond is still there if something fundamental fails, but day-to-day cash is not hostage to punch paint in a back corridor.

Dispute resolution and retainage release

When retainage becomes the battleground for broader disputes, speed matters. Most contracts push unresolved issues into mediation before arbitration or litigation. I have had success carving retainage disagreements into expedited processes. For example, require a meet-and-confer within seven days of a denied release, a short written submission of positions, and a non-binding recommendation from the project neutral within two weeks. The parties can then accept the recommendation or elevate. The surety benefits from this timeline, because completion stays funded while the merits are weighed. Anything that reduces the duration of frozen retainage reduces payment bond claim risk.

Practical signals that retainage is about to become a bond problem

You can usually feel when retainage is drifting from useful leverage to systemic risk. Three signals stand out. First, retainage aging creeps past 120 days across multiple projects. Second, subs begin filing preliminary notices or slow-walking closeout tasks. Third, the project team escalates small document gaps into reasons to hold large sums. When these show up, bring the surety into the conversation early. A brief joint plan for documentation, targeted releases, and clear dates can reset momentum and avoid formal default steps.

A superintendent once told me he considered retainage the “punch list’s paycheck.” He was half right. Teams finish strong when they know they will be paid promptly for finishing strong. They stall when the paycheck feels imaginary. If your retainage policy makes the paycheck feel imaginary, your bond is more likely to be called upon. It is that simple.

A workable playbook

Pulling all of this into a practical approach helps teams align retainage with the protections a contract bond provides without undermining either:

- Set modest starting retainage, then program reductions at objective milestones tied to risk, not calendar dates. Cap retainage by subcontract and allow early release for scopes accepted ahead of project completion. Keep retained funds segregated and visible in project accounting, with aging tracked weekly during closeout. Define tight, documented procedures for requesting, approving, or denying release, with reasons given in writing within a short window. In any default scenario, protect the completion fund first, including retainage. Use it to fuel completion under the surety’s selected option, then settle damages through the contract’s dispute mechanism.

Used this way, retainage strengthens the same outcomes the performance and payment bonds are meant to secure. Owners retain meaningful leverage at the moments that matter. Contractors keep enough cash to maintain pace and quality. Sureties see a path to completion that does not start with untangling months of frozen funds. Most importantly, the project closes before friction turns into claims. That is the point of both retainage and the contract bond, and the line where they should meet.